179

entrepreneurs, by facilitating entrepreneurial development as well as supporting

establishment of new enterprises, and above all, by providing refinancing

facilities in respect of bank loans for industrial activities (manufacturing and

processing) in small, tiny, collage and village industries. The refinance facilities

for the non-farm sector have been sizeable as shown below (Table 5.24):

Based on these refinance support and, more importantly on their own,

the various credit agencies have been rendering ground-level assistance to

the non-farm sector enterprises. The institutional credit expansion for the

non-farm sector, as reported by NABARD, has thus been taking place at a

decent rate of 15 to 20% in each of the past few years. But, the GLC for the

agricultural sector has been growing at a still faster rate. As a result, the non-

farm sector GLC as a proportion of agriculture GLC has been receding in

these years (Table 5.25).

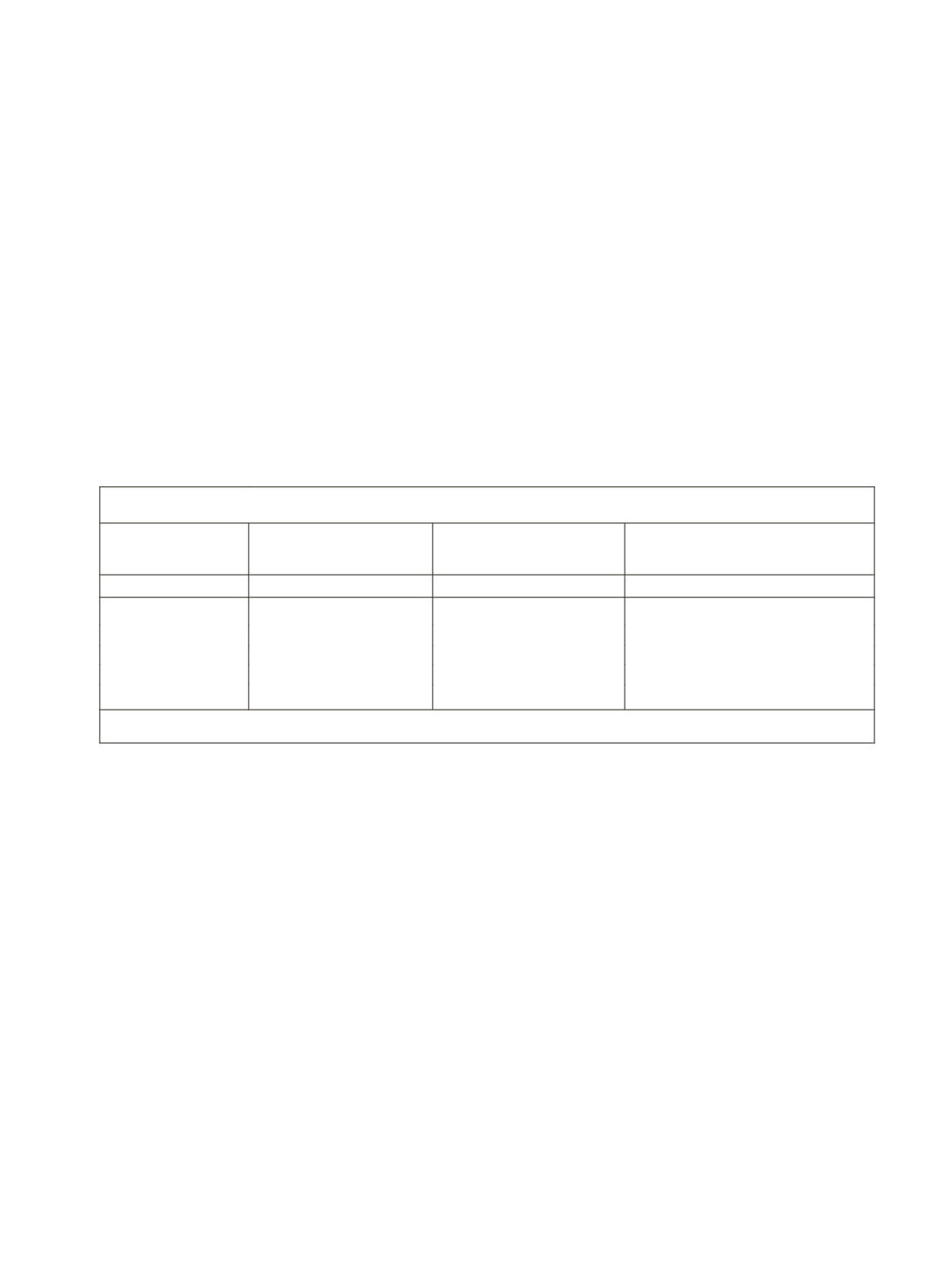

Table 5.25: Ground-Level Credit (GLC) Disbursements for Non-Farm Sector

Year

GLC for Non-Farm

Sector

Aggregate GLC for

Agriculture

Non-Farm Sector as Percentage

of Aggregate Agriculture GLC

(1)

(2)

(3)

(4)

2001-02

16,282

62,045

26.2

2002-03

17,788 (+10.7)

69,560 (+12.1)

25.6

2003-04

20,887 (+17.4)

86,981 (+25.0)

24.0

2004-05

25,042 (+19.9)

125,309 (+44.1)

20.0

2005-06

28,803 (+15.0)

149,286 (+19.1)

19.3

Source:

Special tabulations made available by NABARD for the project. Not available beyond 2005-06.

Regional disparities in non-farm GLC

It is found that regional disparities in the distribution of GLC for the

non-farm sector are truly acute. About 48% of non-farm loans are disbursed in

the southern region alone. With another 24% disbursed in the northern region,

about 72% of non-farm sector loans are purveyed by banks in the two regions

of south and north (Table 5.23); these two regions together account for just

32% of the country’s population or 35% of the rural population or 42% of the

urban population.

Interestingly, the regional disparities in the distribution of non-farmGLC

are much more acute as compared with the distribution of agriculture GLC

(Table 5.27). While about 34%-35% of GLC for are absorbed by the southern

region, the region absorbs 47%-50% of GLC for non-farm sectors. a per the

recent trends, only a fractional deadline in the share of the southern region has

occurred but interestingly, again it has moved in favour of the northern region.