54

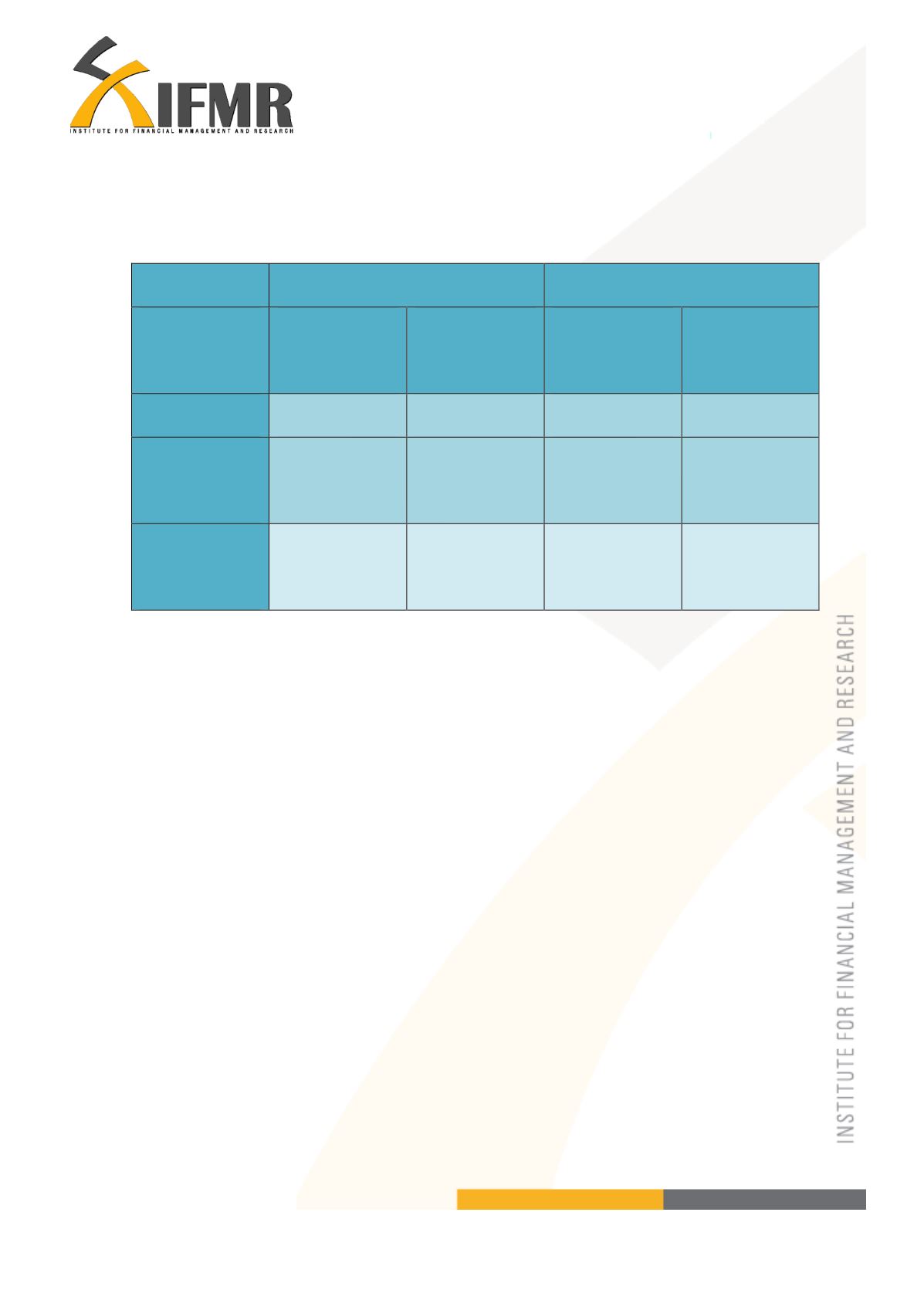

Table 9.2: Karnataka - Savings of the SHG member (monthly and sub-period)

Initial savings

Changed savings

Monthly rate Accumulated

amount

Monthly rate Accumulated

amount

Mean

80.27

3,660.29

100.20

4304.40

Standard

deviation

110.42

2,569.12

98.20

2,255.59

Number of

observations

300

300

300

300

Note that initial savings and changed savings are spread across different sub-periods.

In Karnataka we find from Table 9.2 that the mandatory savings amount remains the

same. Here it seems as though the savings in SHGs is more symbolic and is not being

used for other purposes as in the case of Tamil Nadu.

Hardly 2-3% of the members saved more than the mandated amount in the SHG group.

The top reasons given by them is that

They did not want other members to know that they had extra cash and

They cannot withdraw the money when they wanted.

However, most of the skilled members did save their extra earnings in the form of LIC

policies, fixed deposits, in post offices or in recurring deposits either for educational

needs, contingency heath needs or for a festival. The point to be noted here is the need to